White Labeling Table Funding — Be the Lender, Not Just the Broker

Brendan Boyle, Director of Third-Party Originations at TVC Funding (a division of Temple View Capital Funding, LP), on how white-label table funding lets brokers and correspondent lenders stay the lender of record — owning the borrower relationship — while TVC handles the funding, closing, and assignment seamlessly at the table. Fix & Flip, DSCR Rental, Short-Term Vacation Rental, Bridge, and Ground-Up New Construction product set. National licensing footprint. The model that lets you grow without giving up the client.

Are Cockroaches Lurking in Real Estate Direct Lending?

By Jan Brzeski, Founder, Sage Credit Investment Partners

Commenting on several high-profile bad loans in private corporate credit, JPMorganChase CEO and Chairman Jamie Dimon recently warned that "when you see one cockroach, there are probably more." Although real estate direct lending has gotten less attention than corporate private credit in the current cycle, it is worthwhile to consider some leading indicators for trouble.

When borrowers and lenders wink at each other, watch out

A recent trip to North Carolina gave me pause. I met a homebuilder selling 7–8 entry-level homes a month under $300,000 across central NC. Strong demand, sound model.

The problem isn't him — it's his lenders. Some are offering 90% financing, with a few loans approaching 100% of project cost. Borrowers are quietly coached that they can get even more leverage if they pad their construction budgets, and originators sell this as a feature. It rhymes with the pre-2008 game of musical chairs: everyone knew it would end, nobody wanted to stop the music. This niche is too small to threaten the broader economy, but when borrowers are being guided to mislead their lenders, something is off.

A 95% loan-to-cost loan has no margin of safety

Lenders defend these loans by pointing to experienced borrowers whose finished projects pencil out to a 70% loan-to-value. Fine in theory. But if the borrower stops executing — say, a health issue — the lender can't realistically take over dozens of half-built homes and recover the full loan.

So why does this niche get leverage that apartment buyers and shopping center developers (typically capped around 75%) never see? A few reasons:

Low historical losses. True, but home values haven't meaningfully dropped since this niche emerged post-2008, outside a few Texas and Florida cities.

Houses are liquid. Plenty of buyers, both investors and owner-occupants.

Wall Street loves RTLs. Residential transitional loans have become bond fodder. Once the securitization machine starts humming, standards drop to keep it fed — and bankers paid.

High-leverage fix-and-flip loans: what comes next

The credit cycle is predictable in shape and unpredictable in timing. Standards loosen, then tighten. The question is always when.

Securitization is where the swings show up first. Think of it as cartilage between slow-moving private markets and the instantly emotional public ones. The window stays open for months or years, then slams shut in days. We saw this in 2008 and again after Covid.

When it slams, the most aggressive lenders — the ones living off cheap Wall Street financing rather than their own balance sheets — stop originating overnight. The disciplined players left standing get to reset terms. We don't know what triggers the next reset. We only know there will be one.

What rational investors can do now

Keep a margin of safety. Require real borrower cash. Not every developer wants 100% financing — some have learned that all-leverage careers come with brutal highs and lows. Lending to the slow-and-steady ones often beats chasing the cowboys.

Be willing to grow slowly, or not at all. Capital is plentiful and the temptation to deploy it on whatever terms are available is real. But the same logic that rewards patient developers rewards patient lenders.

Hunt for overlooked niches. Howard Marks calls it second-level thinking — looking past what everyone already sees. North Carolina is growing fast and a great place to live; but with some homebuilder borrowers being handed near-100% financing, there is real risk for whoever ends up holding these loans. The market is wide. There's almost always a "best available strategy" — a corner where you're paid for the risk you're taking, even when the rest of it is frothy.

What's the overlooked niche you'd point to right now?

Jan Brzeski is the founder of Sage Credit Investment Partners (SCIP). To learn more about SCIP, text him at 310-428-9109 or email contact@scipfinance.com.

Liked this read?

Subscribe to Jan Brzeski's LinkedIn newsletter

Get Observations straight from Jan when he publishes — disciplined, operator-first thinking on private credit and real estate direct lending, delivered to your LinkedIn inbox.

By Kendra Rommel, Co-Founder & Principal, Futures Financial

There's a version of private lending that most people in this industry have forgotten. Or maybe they never knew it to begin with…

It doesn't involve warehouse lines. It doesn't involve a capital markets team, a securitization desk, or quarterly earnings calls with institutional partners who are watching your loan tape like hawks. It involves a person or a small group of people who have built real wealth and want their money to work harder than a savings account or a stock portfolio can. And on the other side, there's a real estate investor with a real project who just needs a lender that will actually show up. That's it. That's the whole idea.

Hard money, at its core, was never supposed to be complicated. It was relationship capital. It was trust made liquid. The high-net-worth individual who funded your deal didn't need a rating agency to tell them the collateral was good. They looked at the deal and the borrower and made a decision. Fast, clear, and painless.

Somewhere along the way, many lenders in this space decided that the path to growth lay in institutional capital. And I understand the pull. Institutions can write big checks. They can fund volume that individual investors simply can't match. If you want to scale quickly, that's the obvious answer.

But here's what nobody talks about openly enough: institutional capital comes with institutional demands. And those demands don't always align with what's actually good for borrowers, or for the deals themselves.

When you take on institutional money, you take on their guidelines. Their overlays. Their reporting requirements. Their timelines have nothing to do with your borrower's closing date. Suddenly, the tension between what you promised your borrowers and what your capital source requires you to deliver is real.

I've watched lenders in this space bend themselves into knots trying to thread that needle. They want the production volume that institutional capital unlocks, but they also want to maintain the identity of a true private lender. And more often than not, one of those things wins. And it's usually not the identity.

Our deliberate choice

At Futures Financial, we made a deliberate choice to stay true to the original model. Our capital comes from high-net-worth individuals who understand real estate and risk, and who choose to put their money here because they trust us. That trust is not abstract. It's earned through performance, transparency, and honesty about what we can and can't do.

That means our underwriting decisions are ours. Our speed is real. When we say we can close, we can close. Not because we have a slick marketing message, but because the people who fund our loans don't have a committee meeting to schedule before giving us the green light.

Am I saying this model doesn't have challenges? Not at all.

Building and maintaining a private capital base is not passive work. These are real relationships that require real communication. When markets shift, when a deal goes sideways, when rates move in ways nobody predicted, you don't send an email to an institution. You pick up the phone, and you talk to people. You explain what's happening and what you're doing about it. That takes time. It takes honesty. It takes a standard of accountability that is genuinely harder to maintain than writing a quarterly report.

Volume isn't the same as a real lending business

We live in a market that pushes production at all costs. Volume is celebrated. Big loan counts make headlines. The implicit message is that if you're not growing fast, you're falling behind. I'd push back on that.

Sustainable growth in private lending is not about how many loans you close in a quarter. It's about whether the loans you closed last year are still performing. It's about whether the investors who funded those deals are still your partners. It's about whether the borrowers you worked with came back to you for the next project. Those numbers don't always make for a flashy pitch deck, but they're the ones that actually tell you if a lending business is real.

There's something worth protecting about the way this industry started. The idea that capital doesn't have to be bureaucratic. That a good deal with a capable borrower can get funded by a person who believes in both. That speed and integrity aren't opposites.

We're not anti-institution. We're just pro-relationship. And in private lending, I think that distinction matters more than ever.

The projects that need painless execution deserve a lender whose hands aren't tied. And the high-net-worth individuals who trust us with their capital deserve a team that treats that responsibility seriously, not as a funding source to be optimized, but as a partnership to be honored.

That's the version of hard money I believe in. And that's the version we're building, one deal at a time.

Kendra Rommel is the Co-Founder and Principal of Futures Financial, a private real estate lender offering bridge, fix-and-flip, ground-up construction, and DSCR loans nationwide. Learn more at futuresfinancial.com.

Liked this read?

Learn more about Futures Financial

Bridge, fix-and-flip, ground-up construction, and DSCR loans — funded by people, not committees. Capital that shows up when you need it to close.

Back to Basics: Why Relationship-Driven Real Estate Investing Matters Again

By Nichole Cloud, Director of Business Operations, Rehab Financial Group, LP

Today's real estate market has forced investors to rethink more than just deal structure. Rising interest rates, compressed margins, and slower dispositions are pushing investors back toward something the industry briefly moved away from: relationship-driven business.

At Rehab Financial Group, we've watched this shift happen in real time, and it's changed how we think about our role in the industry.

For years, real estate leaned heavily into automation and digital networking. The efficiency gains were real, but so was the tradeoff: genuine relationships often took a back seat. Investors aren't just looking for financing anymore. They're looking for trusted partners, honest conversations, and people who truly understand their local markets.

The gap Deals on Draft was built to fill

The idea behind Deals on Draft is straightforward: create a smaller, more personal setting where investors, realtors, and industry professionals can have meaningful conversations. While large conferences and industry events still provide value, there's something different about being in a smaller room where people can speak openly about what's moving in a neighborhood, where deals are stalling, and what they're actually seeing on the ground. That kind of ground-level intelligence only comes from the community.

Because at the end of the day, real estate has always been a people business. For most borrowers, their lender exists somewhere behind a screen. They know their sales rep and not much else. At Deals on Draft, that changes. Borrowers get to meet the underwriters, the CFO, and the people who are actively working on their loans and making decisions. They can ask anything. No filter, no formality.

Speed isn't the whole story anymore

Speed still matters, but it's no longer the entire story. Reliability, communication, and experience have moved to the top of the list. Investors want partners who understand how quickly conditions can change and who will work through challenges alongside them, not just show up when things are easy.

That mindset has always been central to how Rehab Financial Group operates, and it's exactly what we continue to hear from investors across the industry.

The response to Deals on Draft has reinforced something we strongly suspected: people still want to do business with people. In-person events create stronger partnerships, more honest conversations, and long-term opportunities that are difficult to replicate behind a screen.

Our next Deals on Draft event will take place on June 25th in Pittsburgh, and we're looking forward to continuing to build meaningful connections within the real estate investing community.

Technology will always have a place in this industry, but long-term success will belong to professionals who can combine modern efficiency with strong personal relationships. The investors best positioned for long-term success will be the ones who continue showing up, building their networks, and staying connected to the communities where they invest.

Sometimes, the smartest move is simply getting back to basics.

Nichole Cloud is the Director of Business Operations at Rehab Financial Group, LP — a direct private lender specializing in financing for real estate investors nationwide.

Liked this read?

Learn more about Rehab Financial Group

A direct private lender for real estate investors — built around the kind of relationships, decisions, and execution that don't live behind a screen.

The Economic & Housing Market Update — and what a Stech Family Office–style investor does about it.

By Dave Stech, Stech Family Office

Let me start by saying: I spent way too many years in corporate America.

And yeah, I was in senior leadership at places like Kodak and Disney…which had its perks. But I also had zero freedom.

And here's the part that hits a nerve for a lot of high-achieving professionals: my problem wasn't ignorance. It wasn't laziness. It was comfort. I was successful enough to stay where I was…but boxed in enough to hate it.

When I finally did leave, it was a clean break—except for one thing: I had to figure out what to do with my 401(k). A well-meaning friend referred me to his broker at Merrill Lynch and I transferred the whole six-figure sum.

I'll spare you the gory details. Let's just say I learned a lesson the hard way.

That's how I'll start today: one win, one lesson—because if you're reading this, you're probably someone who has achieved "success" inside someone else's system… and you're realizing the same thing I did:

You can't delegate your family's financial future to people for whom there's no downside. No consequences. You have to control it yourself.

A quick look back: why my State of the Union is worth your time

My first "State of the Union for Real Estate Investors" was at Harvard 21 years ago.

In 2005, I showed them my research and said, "Get out," and they basically laughed me out of the room.

In 2008 (after it turned out I was right) they invited me back and I told them, "I'm going ALL-IN in Vegas!"

In 2011, after Vegas became the #1 buy-market in the country, they asked me back again and I said: "Go ALL-IN everywhere!"

Those weren't guesses. They were cycle calls—based on the kind of market timing and macro pattern recognition that's been the backbone of how our family invests.

And somewhere in the middle of all that, something bigger happened: my sons joined me. We became the Stech Family Office. And now I get to do three things every day, with my sons: Make Money, Do Good, and Have Fun.

Not long ago, I was introduced at a conference as "the head of the most successful private lending family in America." I remember thinking, wow… look how far we've come in such a short period of time.

And then I had the sobering thought that frames this entire article:

What you don't know, your kids will inherit.

That's not a motivational quote. That's a generational law. So keep reading. :)

Part 1: The Economic Update

The "shape" of this economy isn't a single story

If you're waiting for the economy to feel like one coherent storyline again, you might want to grab some crossword puzzles or something. It's likely going to be a while.

Because this cycle isn't one wave. It's a set of lanes moving at different speeds… and the separation between those lanes is widening.

In other words, there's a strong argument the economy isn't simply "strong" or "weak." It's split.

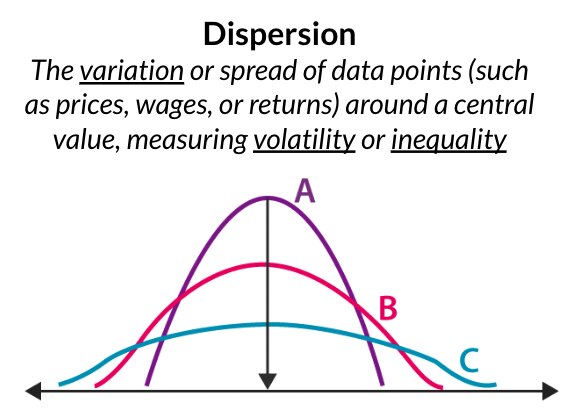

The technical word for the split: dispersion

In the same economy, outcomes can disperse. They spread out.

High dispersion = high variability

Low dispersion = high consistency

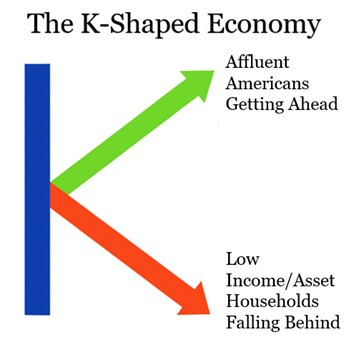

When dispersion is high, you get big gaps in outcomes across households, companies, and asset classes—all at the same time. In other words, a "K-shaped" economy.

And once you see that, you stop asking, "Is the economy good or bad?" (a low-resolution question). You start asking, "Which lane am I in—and what lane am I building my strategy for?"

The K-shaped economy is real (and it's not subtle)

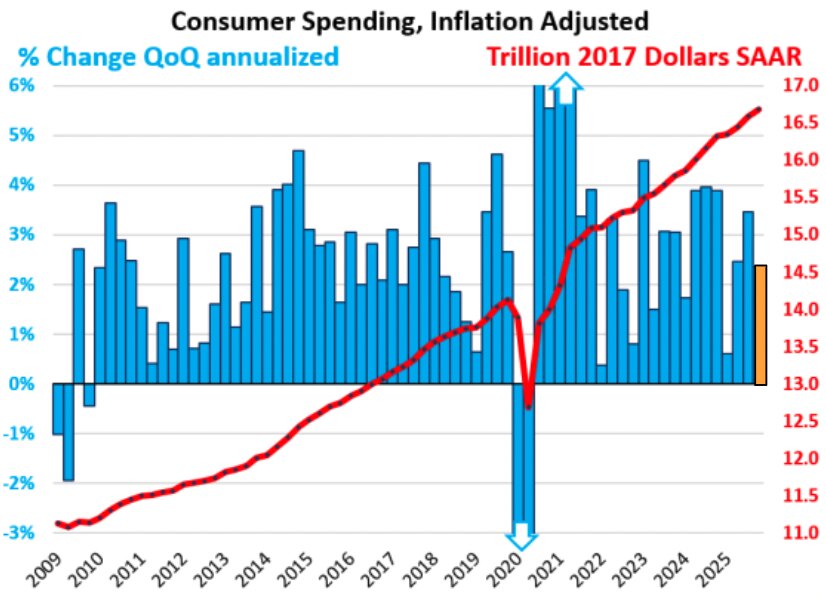

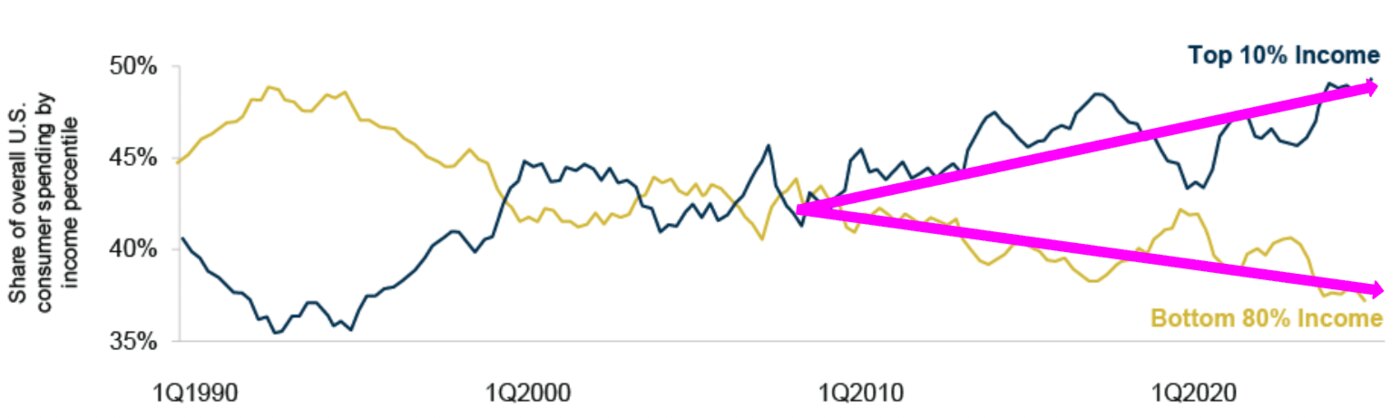

Look at consumer spending. In the aggregate, spending can look "fine," in the sense that it continues to stay positive quarter over quarter (as it did in Q1, in orange).

Source: WolfStreet

But underneath, you can see the K. A narrow cohort is carrying the load: the top 10%. The top 10% of income earners now account for 49% of all consumer spending.

Source: Oaktree Capital

And if you're a high-income professional, business owner, or investor… there's a good chance you're in that cohort. That's not a flex. It's a warning. Because it means:

one part of the economy continues to spend and invest,

while the broader population is increasingly forced into trade-offs.

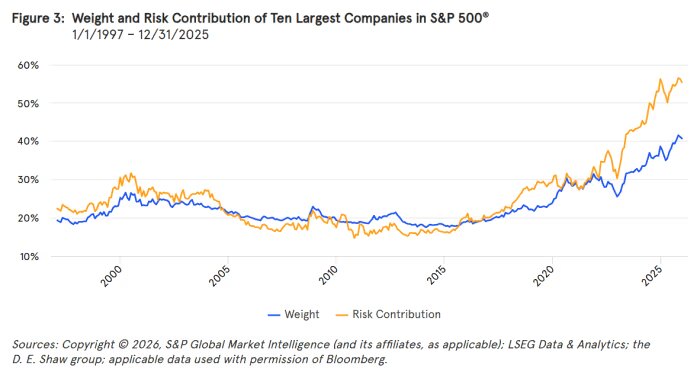

The stock market is split too

You may own "500 stocks"… but your outcome is not diversified.

Most people look at the S&P and think: index = safety. But in a high-dispersion environment, even "the index" can become a concentrated bet.

As you can see here, market breadth is shrinking; the top 10 largest companies now make up 40% of the S&P's "weight" (in blue). And even more troubling, the top 10 make up 56% of its "risk contribution" (in orange) — meaning if the S&P moves tomorrow, more than half of that move is coming from the top 10.

When the market is cap-weighted and a handful of mega-caps keep getting bigger, you get what I call: the diversification illusion. You own 500 companies… but your outcome is increasingly dominated by the same crowded trade.

And the internal market math is screaming that reality:

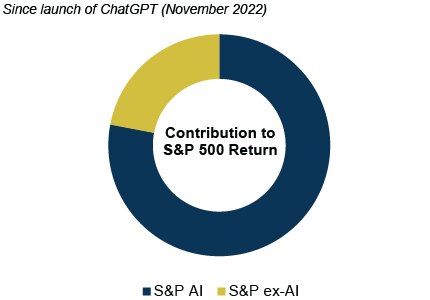

A small group of AI-related names has driven over 75% of overall returns since the launch of ChatGPT.

If you strip out the Information Technology sector (where companies like Nvidia, Microsoft and Apple reside) and Communication Services (home to Google and Meta), the S&P would have only returned 6% in 2025.

Source: Oaktree Capital

So the question isn't "Is the stock market up?" The question is: How much concentration risk are you pretending you don't have?

Because when leaders wobble, the entire index starts behaving like a single position.

The Fed is back… quietly

The "Sneaky Fed" and a new sheriff.

After nearly four well-publicized years of quantitative tightening, the Fed has been adding to the balance sheet again—quietly, steadily, and on purpose.

When they do this—when the Fed buys short-dated government debt and credits reserves back into the banking system—you can call it what it is: liquidity support. A form of quantitative easing… even if they don't shout it from the rooftops. They're trying to prop up markets (and GDP) without calling it stimulus.

Now here's the twist: the Fed is likely in for a shake-up here soon. The new Fed Chair—Kevin Warsh—is looking more hawkish, more interested in Fed independence, and more willing to keep interest rates high in the name of controlling inflation.

Whether or not you agree with any one political storyline, the investment takeaway is simple: Don't build your financial strategy on "the Fed will save us."

Historically, easing cycles take years to play out, and they're often messy—rates can go down, then back up, then down again. And even with cuts, you can still live in a world where money isn't "cheap," credit isn't "loose," and borrowers still pay up for speed and certainty.

Hope is not a strategy, as the saying goes.

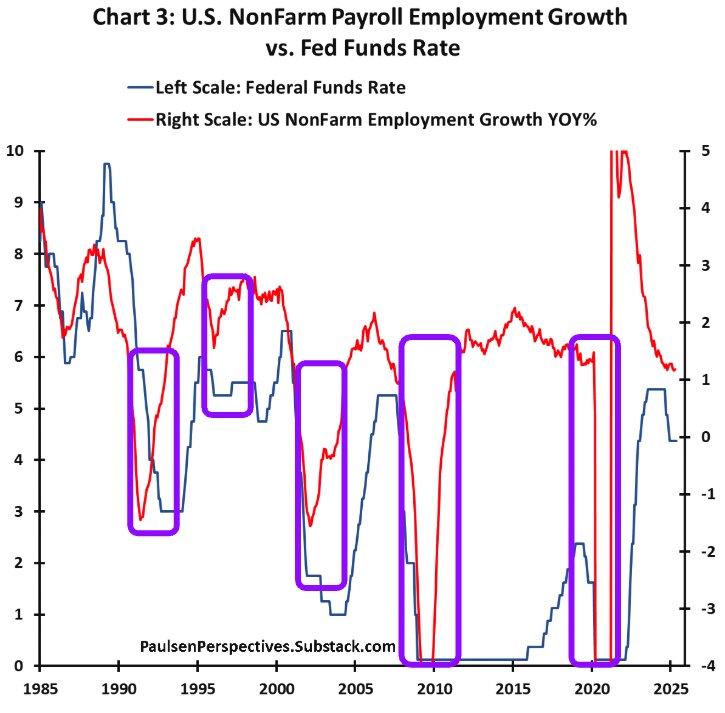

The labor market: why the script isn't working this time

There's a simple mental model most people carry vis-à-vis interest-rate policy and the labor market:

That intuitive chain of cause-and-effect has basically held true for decades.

Which is exactly why this cycle is confusing everyone: the first part of the script happened… but not the latter.

Easing shows up first in financial conditions and market pricing. But the labor market only truly re-accelerates when employers regain hiring intent. And right now, that intent is not coming back the way the old model says it should.

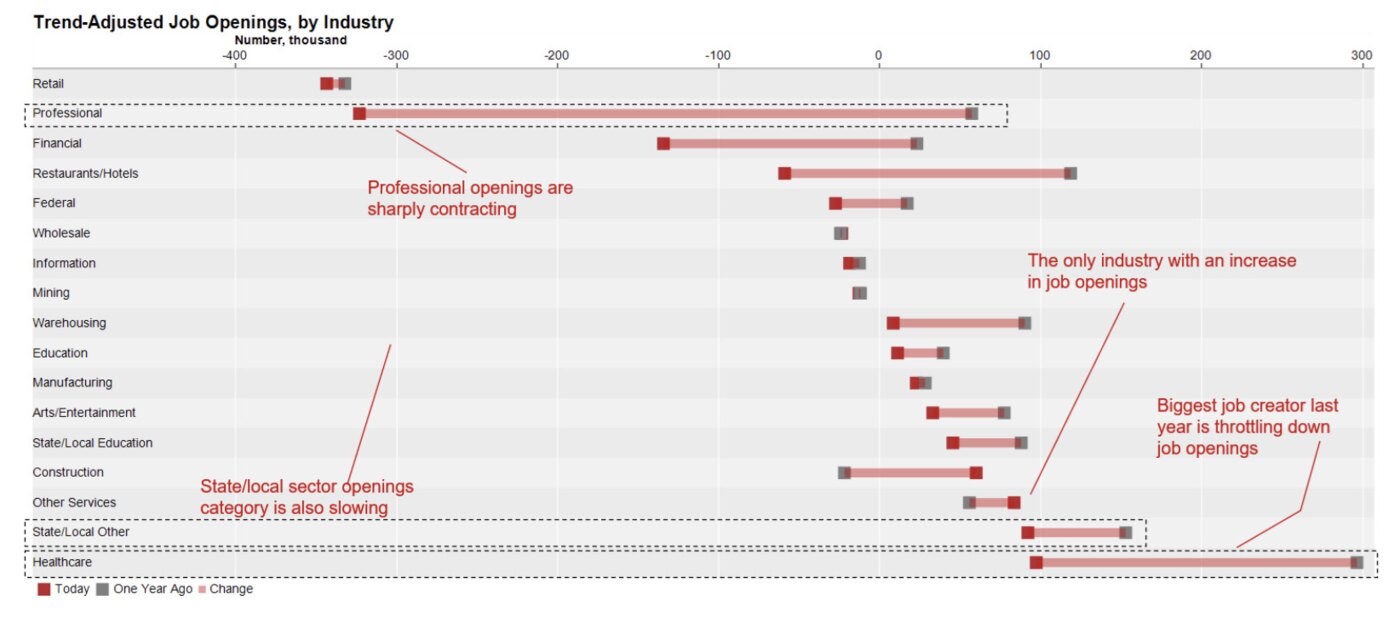

If we break it down by sector, on a "trend-adjusted" basis (i.e. a "difference from normal" basis)… job openings today are down compared to openings a year ago in 14 of the 17 major sectors.

Source: Mauldin Economics

Even the healthcare sector—responsible for ~53% of all hiring over the last few years—is throttling down job openings.

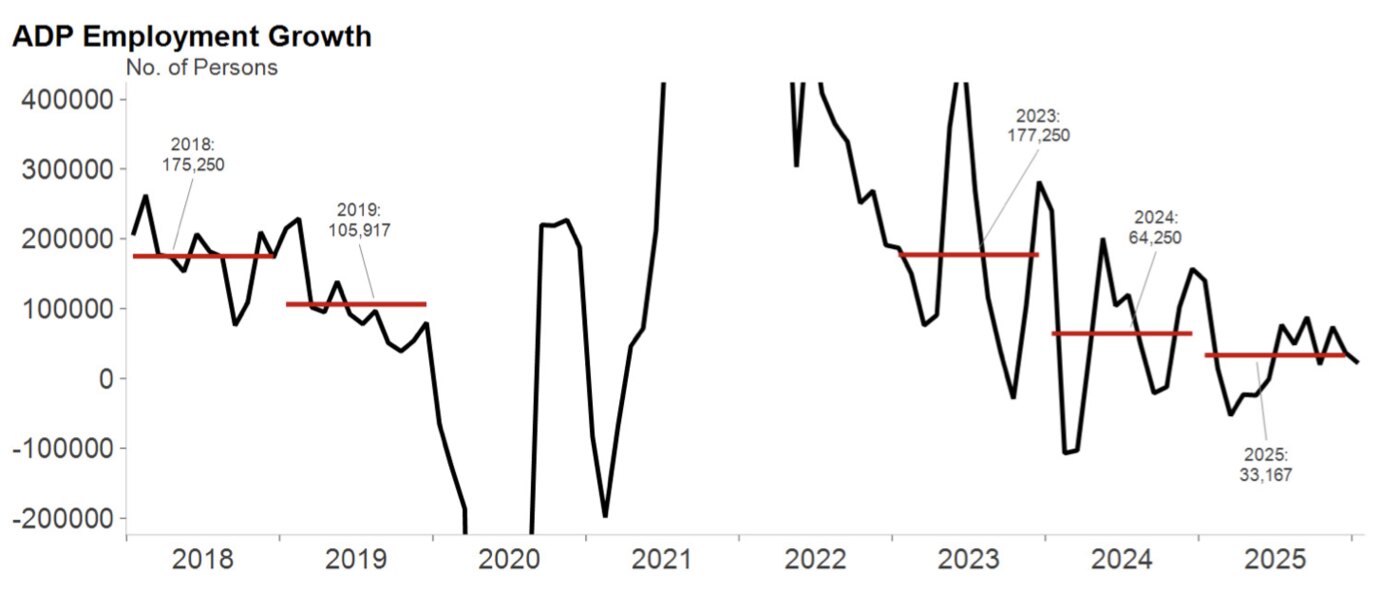

Bottom line: excluding the post-pandemic volatility years of 2020–2022… 2026 is shaping up to be the slowest year for job growth in a long time.

Source: Mauldin Economics

It's simple technical analysis: the averages step down from ~177K (2023) to ~64K (2024) to ~33K (2025). That is not "still strong, just cooling." It's now a different operating speed.

From a technical-analysis standpoint, once you're in a low-growth channel, you tend to stay there until something forces a reset.

Will more easing force a reset? Eventually, yes, it probably will. But only if the current low-growth channel is primarily a rate/credit-demand problem.

If it's a "structure" problem (i.e. an increasingly K-shaped economy where growth is concentrated, incremental spending goes to capex over headcount, and uncertainty keeps firms cautious), you can have plenty of easing and still not get the labor reset you're looking for.

Part 2: The Housing Market Update

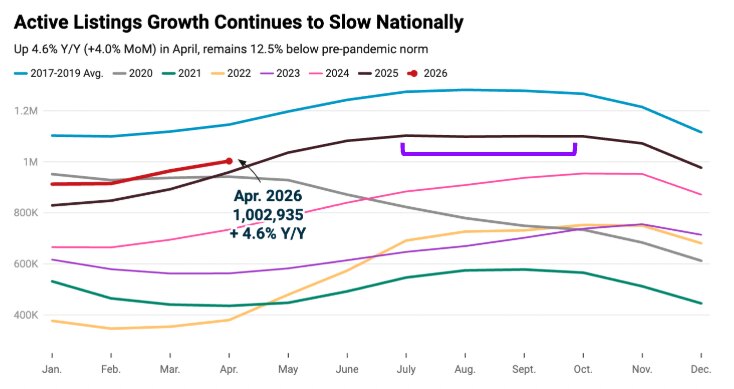

Supply is rising… but the market found a "low-liquidity equilibrium"

Inventory (active listings) has been growing—but the pace has cooled meaningfully. And then something unusual happened: active listings basically flattened for a long stretch in the back half of 2025.

Source: Realtor.com

That "flatline" is a clue. It's the market adapting. Not by blowing inventory out… but by shifting into what I call a low-liquidity equilibrium.

A low-liquidity equilibrium is when the market looks balanced on paper, but only because both sides are constrained—and nobody feels any urgency to blink.

Optional sellers throttle supply because they don't want to give up their mortgage rate (and then overpay for the next house at today's payment).

Buyers ration demand because the payment is punitive. They either can't afford it, or they refuse to.

So sales happen at the margins: concessions, price reductions, negotiation, and time—rather than through high transaction volume.

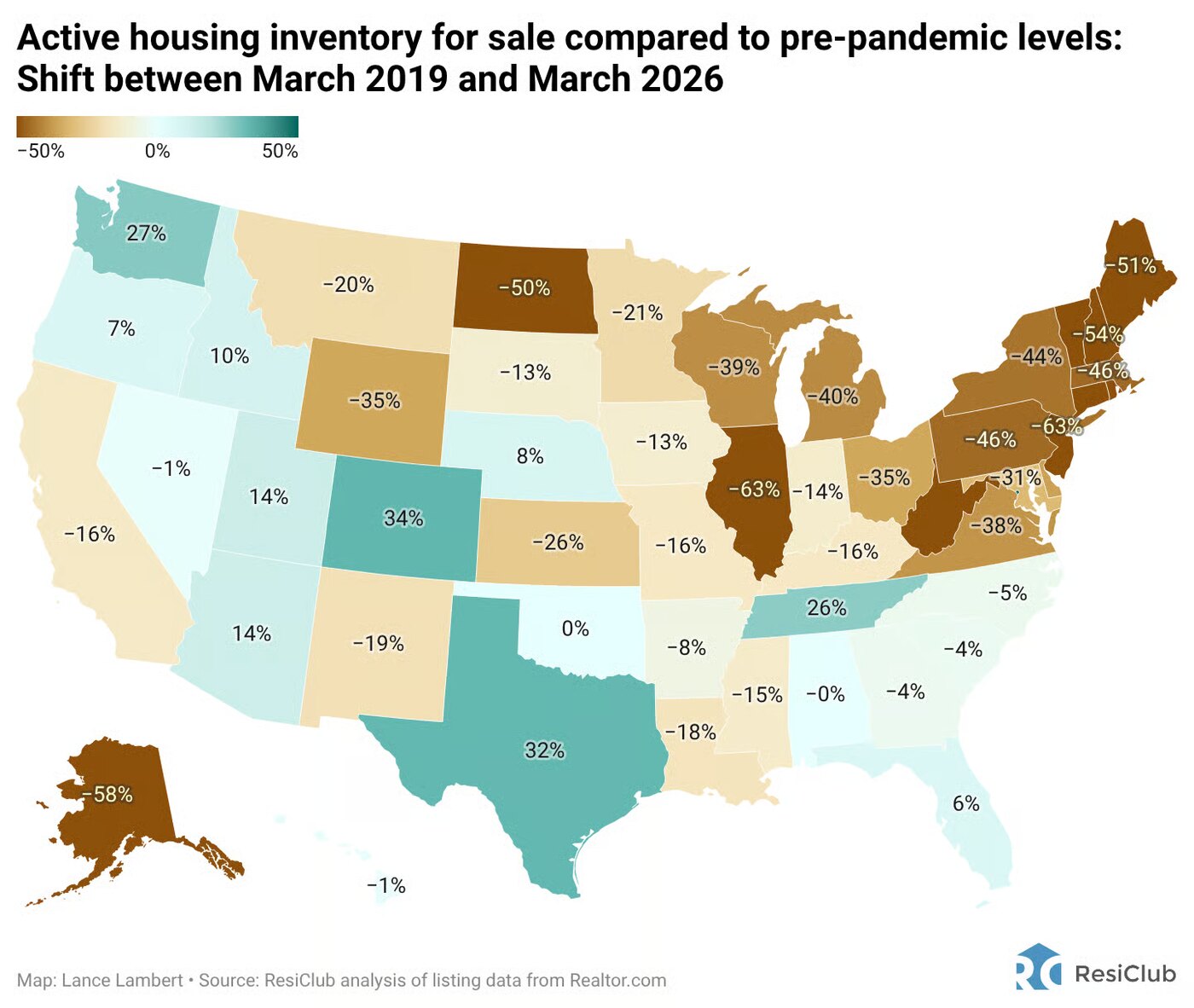

So yes, inventory is up. But remember, the market is rebuilding supply from a historically starved baseline.

Source: Resiclub Analytics

So two things can be true at once:

We can still be below pre-COVID inventory norms (as we are nationally, and in all the brownish states above),

But the market doesn't feel like a seller's market. It feels more like a buyer's market: low-intent, low-demand, and sluggish.

Demand is sending mixed signals: the funnel is leaking

The housing demand "funnel" is not one number. It consists of three core stages, each with its own metrics.

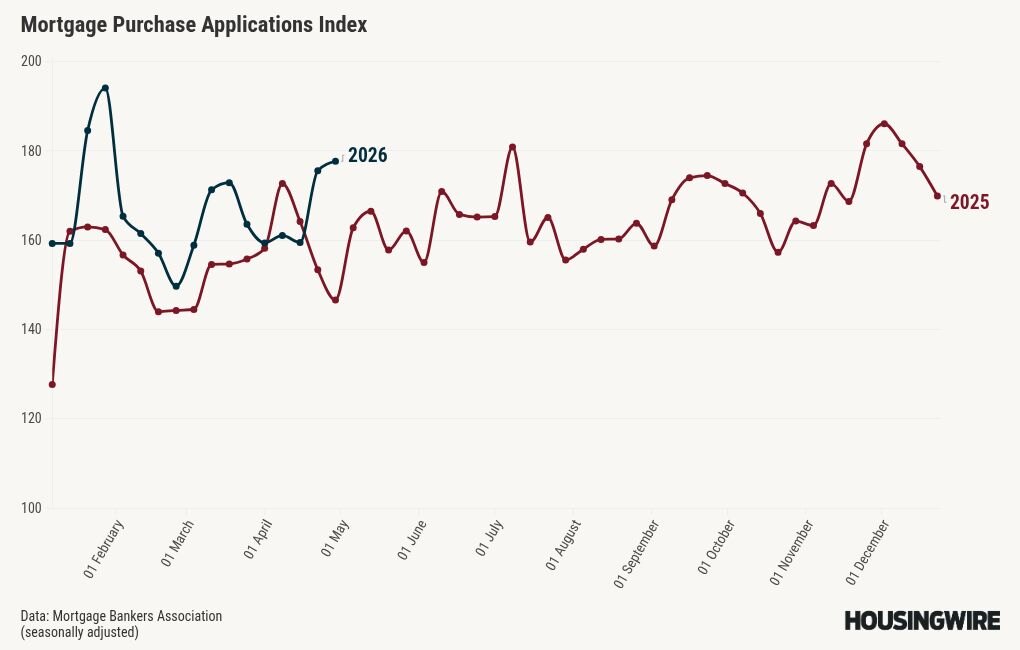

Financing intent (mortgage applications) typically improves when rates improve. And that's played out for most of 2026: applications have been mostly above the 2025 pace for most of the year.

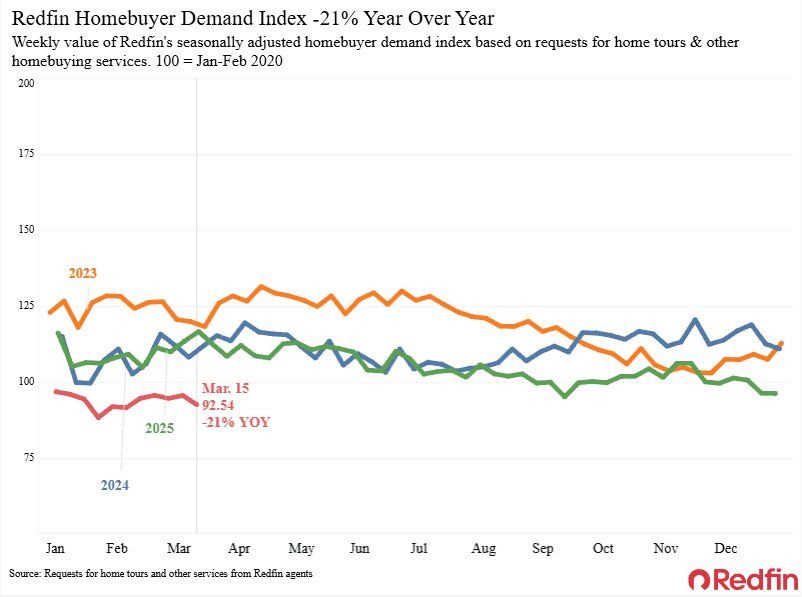

But "on-the-ground" shopping can stay weak because people run the payment math and bail. And that's what we've been seeing: Redfin's Homebuyer Demand Index—built off requests for tours and other homebuyer services—is down -21% YoY, which is as low as it's been at any point since COVID.

To be clear, these are people raising their hands, not just poking around online. As of mid-March, there are 21% fewer of them than there were when interest rates were ~100 bps higher.

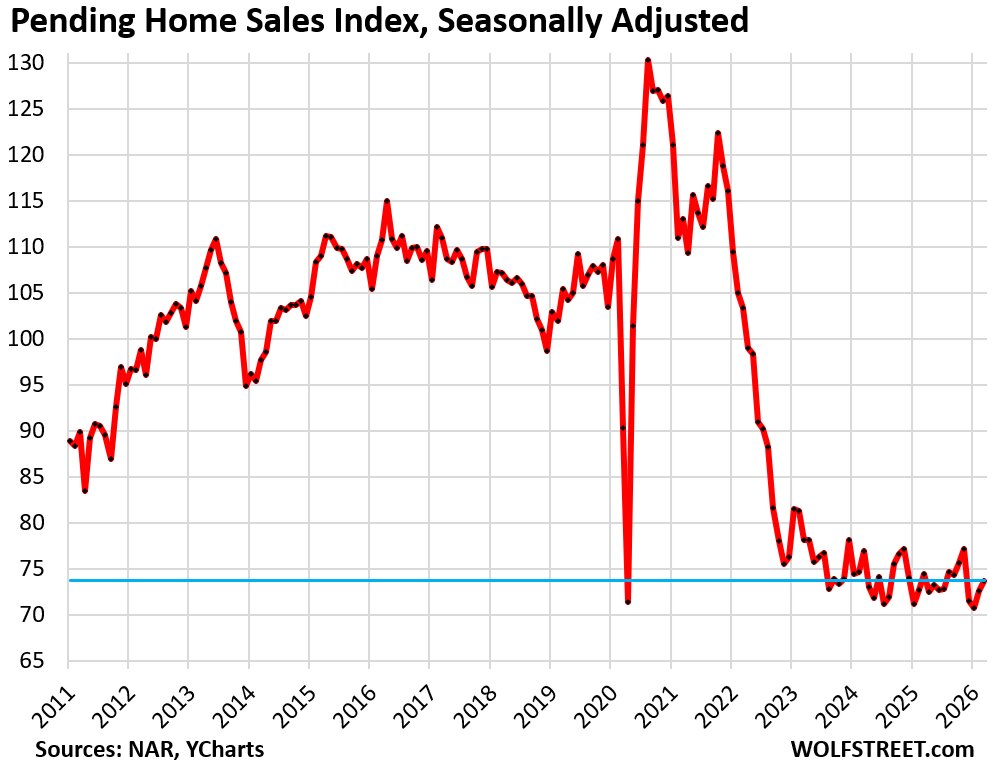

Signed contracts (pending sales) are the final piece of the demand funnel.

In a word, they're looking anemic—near record lows as of Q2'26. And the reason is pretty simple: sellers are anchored to yesterday's price, and buyers are more conditional.

So you end up with a market where more people re-enter at the top of the funnel, but fewer people make it through the bottom. That's not a booming market. That's a low-liquidity market.

Why flippers matter: they're the "edge indicator"

Fix-and-flippers represent a minority of total sales, but they matter because they're the definitional "marginal" participant.

They operate on:

thin time windows,

tight spreads,

and hard constraints.

They're forced to react faster than owner-occupants. So when you want to know where price discovery is heading, flippers are often the canary in the coal mine.

And the data tells an interesting story:

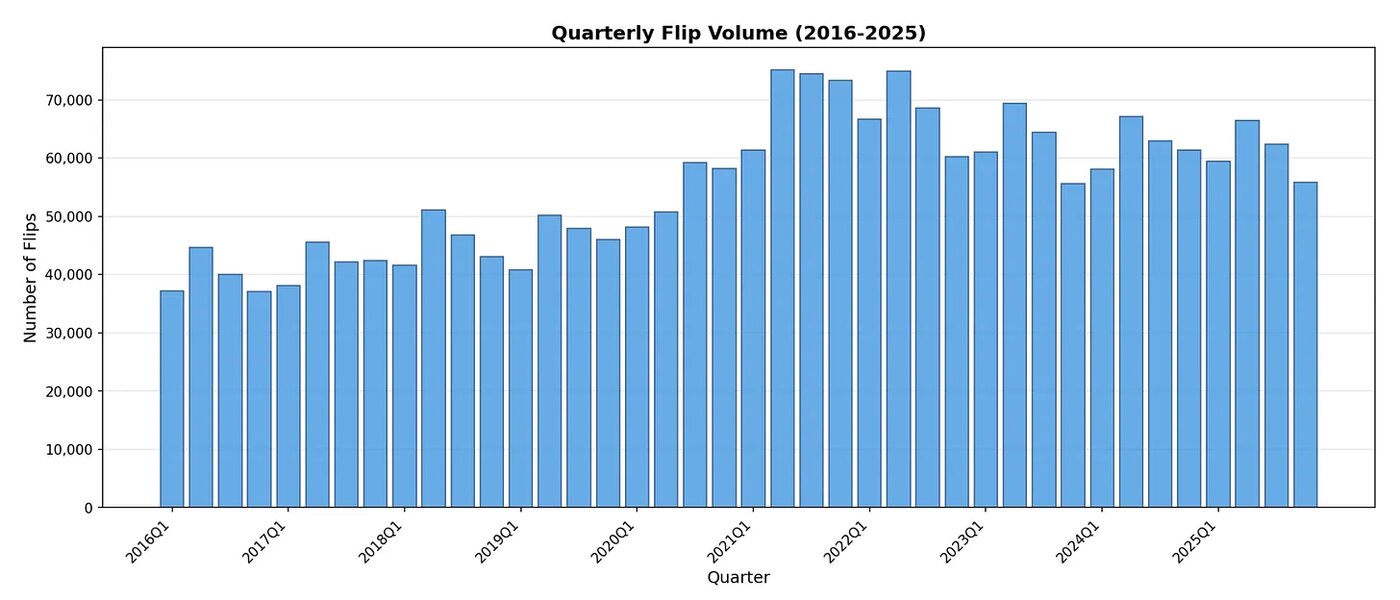

Flip volume has cooled from the peak but stabilized above pre-2020 baselines.

Source: SFR Analytics

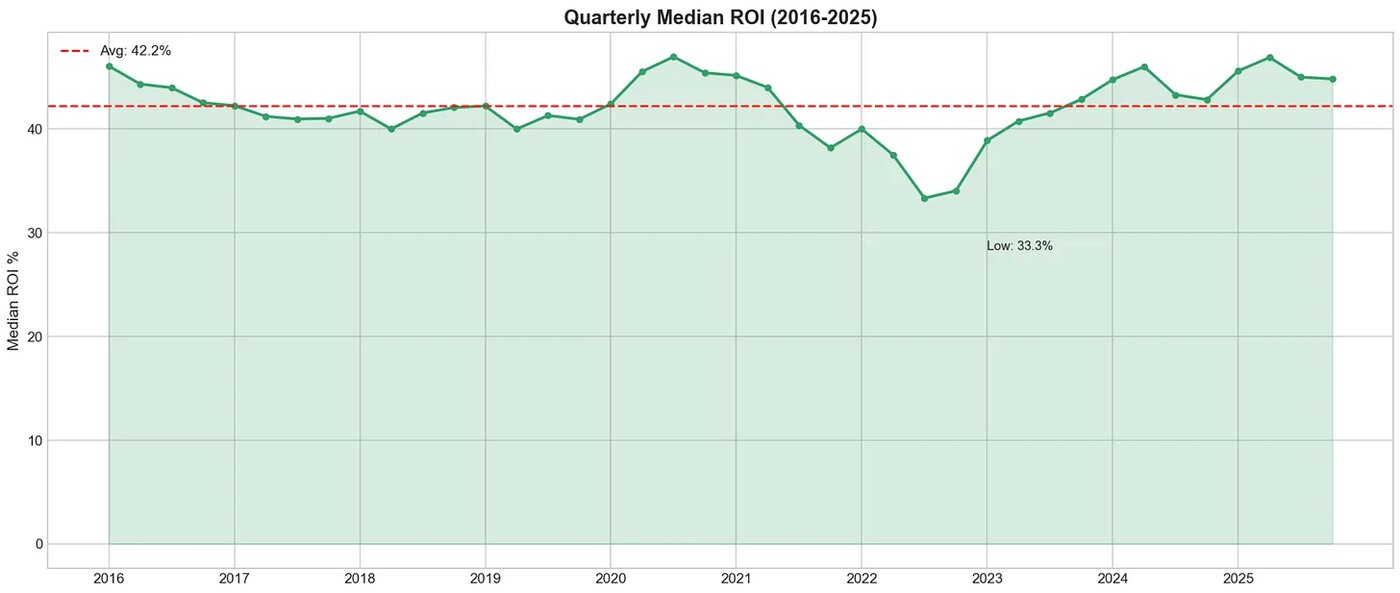

Gross ROIs have trended toward historic highs.

Source: SFR Analytics

Which sounds counterintuitive: how can flippers be profiting more in this tighter market? Well, you have to remember what flipping really is: it's a spread business.

When rates rise and the market gets choosy, a lot of amateur, "light-rehab" operators step back. That can reduce bidding pressure on the "ugly" inventory… where many of the true pros live.

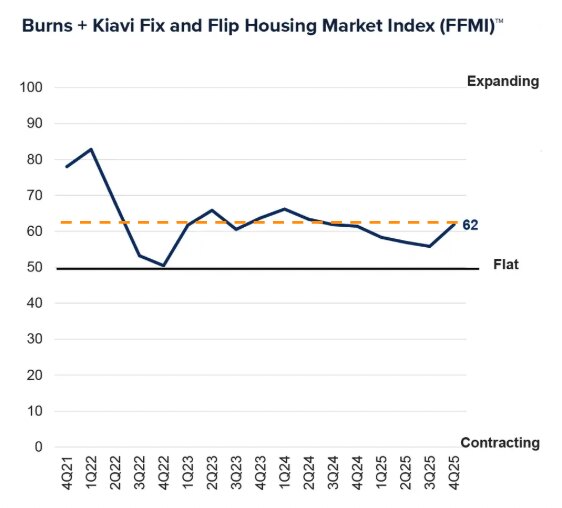

And sentiment among flippers improved toward the end of 2025, with many expecting to do more throughout 2026.

Source: JBREC

At an index score of 62, flippers are saying they're more optimistic about the market than they've been at any point in the last 6 quarters (since 3Q'24). In fact, this uptick is the largest quarter-over-quarter jump in 3 years.

As a private lender, that's music to my ears, because it signals something simple:

Active operators still need capital—and they'll pay for velocity and certainty.

The real conclusion: what do you do with this?

Let's cut through the noise. As an investor, there's one thing we can all agree on:

It is incumbent upon you to make the best risk-adjusted decisions you can at every point in the market cycle.

So ask yourself the question we ask ourselves:

What ONE passive investment strategy do you truly believe in right now? What asset class do you have real conviction will generate passive, recurring income with controlled risk in an overpriced, overheated, uncertain environment?

If you don't have that answer, that's not a character flaw. That's just information.

So let's talk about the options objectively:

Stocks? Uncertain—and increasingly concentrated.

"Alternative" assets you don't understand? If you don't control the outcome and you don't know who's pulling strings, you're effectively gambling.

Commercial / multifamily? There may be distress—but most people don't know what they're doing there, and the distress cycle isn't necessarily finished.

Single-family rentals near a market peak? The effort-to-return equation is worse than most people admit, and the old "rules" don't pencil the way they used to.

But there is one strategy that benefits from an environment where:

money isn't cheap,

underwriting is tighter,

and borrowers still need speed and certainty.

That strategy is private (hard money) lending.

Here's the principle

Smart real estate investors pivot throughout a market cycle to optimize risk-adjusted returns.

When the market is at or near peak conditions, we shift away from owning more long-term exposure… and toward controlling real estate short-term. Because when you control real estate rather than own it:

you reduce exposure to downside price risk,

you can still generate double-digit, passive, recurring income (often interest),

and you keep your capital liquid—ready to redeploy when a better opportunity presents itself.

And yes—there are always deals in every market. But in a market like this, great deals are needles buried in haystacks of risk.

So here's the better question:

Wouldn't it be better to find a haystack… where the needles come to you?

That's what being the bank is.

So what should you do next? (3 moves)

1) Make the economy your economy: win The Money Game

Your goal isn't to predict the next headline. Your goal is to build a personal system that does what our Family Office system does:

Generate cash (aka income),

Accumulate wealth (in the form of assets that both throw off cash AND go up in value),

Keep more of both (legally and intelligently, through vehicles like Self-Directed IRAs),

And steadily improve your effort-to-return ratio.

2) Go get the free library (and the advanced ebooks)

Go to justbethebank.com/vault for our Family Office's library of free resources, including three advanced ebooks I've written on private lending—over 100 pages of the most valuable, most ready-to-implement material I've ever put on paper. Yours, FREE.

3) Get on the Market & Investment Alerts list

If you want ongoing research, updates, and investor-grade market insights—get yourself added to the alerts list so you're not relying on the news cycle (or your broker's hot takes) to make decisions.

Dave Stech is the founder of the Stech Family Office and Just Be The Bank. To learn more, visit justbethebank.com.

Want more from Dave?

Visit Just Be The Bank

The Stech Family Office's home for private lending research, free ebooks, market alerts, and the live State-of-the-Union webinars Dave has been running for 21 years — from Harvard '05 to today.